According to Wikipedia, in complex analysis an essential singularity of a function is a "severe" singularity near which the function exhibits extreme behavior. The category essential singularity is a "left-over" or default group of singularities that are especially unmanageable: by definition they fit into neither of the other two categories of singularity that may be dealt with in some manner – removable singularities and poles.

---------------------------------------------------------

No need to panic, a lot of analysts tell us, since far from being on the verge of some earth shattering event Japan has invented the economic equivalent of a mechanical perpetual motion machine. Or as Nobel economist Paul Krugman put it recently, “while there is much shaking of heads about Japanese debt, the ill-effects if any of that debt are by no means obvious”. Maybe there is just one word missing here - yet.

This, however, will not be the viewpoint taken here. The rise and rise of Japanese debt is far from benign, and the dynamic, we are convinced, will at some point become unsustainable. Unfortunately by the time we reach that point it will be too late. Indeed, given that we agree with Krugman that the underlying cause of Japan’s malaise is demographic, after several decades of ultra-low fertility in all probability it already is too late. The root of the problem is, as he says - wait for it - that there is "a shortage of Japanese".

Far from being like that woeful economist so tellingly characterised by Keynes, the one who through many travails and pages and pages of equations is only able to tell us that when the storm is long past the ocean is flat again, we feel we have more in common with the character so ably played by Mike Shannon in the Jeff Nichols’ film “Take Shelter” - "there’s a storm comin, one like none of you have ever seen before…."

If You Print Your Own Money, And You Run An External Surplus, How Can There Be a Problem?

Japan’s problem is benign, so the argument goes, since the country has an external surplus, and can print its own money. As a result there is a savings surplus, and no problem selling government debt, even at ridiculously low interest rates. And since the interest paid remains ridiculously low, then there is no problem servicing the debt, and if there ever was, why then the Bank of Japan could just buy even more of its own government bonds, effectively driving the interest rate even lower. In theory there is no good reason why it couldn't even follow the lead being currently set in Germany, and push the rate into negative territory. Heck, the government would then be even earning income on its debt. It would be a good investment.

But somehow or other this view fails to convince. In particular it fails to get to grips with why Japan has gotten into this situation. It also doesn't offer any kind of road-map for how the country could ever get back to the sort of monetary regime that was once widely considered to be "normal". Or perhaps, in the world we now live in, as the US novelist Thomas Wolf once put it "you can look homeward angel" but in fact "you can never go home again". Which is just a very poetic way of saying that time has an arrow, and that some processes are irrevocable and irreversible.

So, if this is what you were hoping for, then bad luck, since there is simply going to be no such thing as a return to normality for Japan. That being said, what we have to avoid at all costs is Japan becoming the "new normal", the text book case of a society where the fundamental mismatch between declining demography and appeasing an ever older electorate with populist politics leads to complete dysfuncionality, a dysfunctionality which is then reiterated in one country after another. From this point of view it is fascinating to note just how fast Japan is getting towards "the end of the road". Some investors have even been getting ahead of themselves and frantically shorting Japanese debt in the anticipation of future and continuing credit downgrades, without asking themselves the really awkward question - what happens to the country if it is eventually forced to default on its debt.

If on the other hand we are able to see that something is going on in Japan which is neither normal, nor desirable, nor sustainable, then we just might like to ask ourselves what then gets to happen next? Certainly there is nothing in conventional economic theory which can help us anticipate the answer, since this kind of end of the road point has not been foreseen, anywhere.

It’s equally fascinating that so few people are really talking about this development at the moment. The assumption that things can more or less go on and on is widespread both in and outside Japan. Despite the frequent references to "Japan's lost decade", the country has now lost not one, but two - what was it Oscar Wilde said, losing one child could be an accident, but losing two surely has to constitute negligence - and as things are shaping up we seem to be all set to have a third one in front of us, markets and weather permitting, always assuming the Japanese government remains able to finance its debt.

Yet at the moment there seems to be no danger of that. Japan has become flavour of the month among investors, following the continuing verbal interventions from prime minister Shinzo Abe. Against all odds, people are buying the story that an inflation target of 2% is attainable, and that the country can permanently devalue its currency by a sufficient amount to produce an ever larger trade surplus, despite the war of words that has already broken out about "currency wars". Or perhaps it has become convenient to believe the impossible will be possible, simply to make money on short term trading positions. Given the quantity of long run uncertainty, this seems to be the main obsession of markets right now, following the dictum of the 1960s philosophy made famous by Jack Trevor in the film "Live Now, Pay Later."

A Country Growing Short Of People?

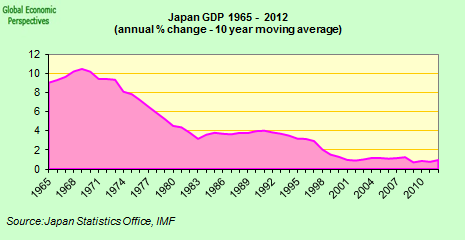

But let’s keep the debt issue for later and start with the demography – here Japan is certainly a real global leader, in this case for its advanced population ageing. Japan is not only an ageing society: It’s THE ageing society. Following decades of an ultra low birth rate and negligible immigration, it faces a steady decline in its working-age population and a rising dependency ratio for decades to come. There is no changing this now. Even some "miracle" reversal of the fertility problem would take decades to work through, so whatever happens next, things will get worse before they get better.

Japan's population - in median age terms - is the oldest on the planet. Median age is around 45, and it will continue to rise. There is no real prospect of it coming back down again, since the process it is experiencing appears to be totally irreversible. Forecasts see the median age in Japan rising to more than 50 within the next two decades, and really here we are breaking totally unknown territory – no society in the whole of human history has ever been this old.

Given this prospect, it is natural to expect that the country should save heavily to make provision for the future--and it does. But a country with an ageing and declining workforce gets an additional problem, one of structural demand deficiency due to the changing balance between saving and borrowing. Investment opportunities in Japan are limited, so that businesses will not invest all those savings inside the country itself. The only surprising thing is that people are still surprised by this.

This demand deficiency results in a process we have come to call export dependency (leveraging the global rather than the local economy in the search for customers). Japan has now well passed the threshold at which the economy, as a modern market economy, can rely on domestic demand and domestically oriented investment to grow. The trouble is, that given its export sector cannot grow fast enough to keep pace with the contraction in private internal demand, the country has become increasingly dependent on large fiscal deficits to keep the ship right side up.

However contrary to the expectations of the classic life cycle model, the conclusion we have come to is that rapidly ageing societies will not, in the main, be characterised by aggregate dissaving but rather by the fight against it. In the context of international capital flows this means that rapidly ageing economies will be characterized by an external surplus and not, as theory would predict an external deficit. According to the said life cycle theory, savings by consumers should not affect total aggregate savings in the long run because savings today, by definition and through the idea of consumption smoothing, turns into consumption tomorrow. Yet this might be the wrong way to read the life cycle hypothesis: ageing may be associated with the propensity to run an external surplus and this may lead a country to a state of export dependency.

The conclusion we draw from the above is a simple one – if Japan is going to see a decline in working population over the next several decades (and possibly much longer, since so long as fertility remains below replacement rate each generation will be smaller than the previous one) and if this lies at the heart of the deficient domestic demand deflation problem, then it means the issue is a deep structural one which won't be resolved by any kind of "kick start", however large. The only consequence of having permanent fiscal injections will be not to give stimulus, but rather an accumulation of debt that will be increasingly harder for those smaller and poorer workforces to pay down in the future – especially if the process is associated with ongoing deflation.

To use an analogy - it isn't simply a question of a planet which has slipped off or strayed from its orbit (or “good equilibrium”), and just needs a nudge to get it back on, what we have is a planet which has veered off onto a whole new trajectory, one which leads to who knows where. This situation was never contemplated by the founders of neoclassical theory, and yet, having started in Japan, the phenomenon is now extending itself steadily across all developed economies in one measure or another.

As long as Japan is the only guy in town facing this kind of problem, there is a simple solution - invest national savings abroad, in countries where populations are younger and still growing, and returns on capital are surely higher. These other nations should be able to pay back loans when they are richer and older, supplying some of the funds needed to meet Japan’s pension promises and other obligations.

Up to the arrival of the global financial crisis Japan played this game well because it was the only one playing it. The problem is that now every single OECD economy, one after another, will steadily be looking to do the same. So in similar fashion, those who urge a solution to Europe's imbalances via an increase in German fiscal deficits to stimulate consumption miss the point: arguably what people in these societies need to do is save more, not less, and certainly when it comes to the public sector.

External demand and foreign asset income become crucial elements of growth for ageing societies, and if we end up with every developed country trying to export its way out of the mess it is surely not going to work! The first signs of this can already be seen in the Euro Area, where the sterling attempts of the countries on the periphery to escape from their trap through the ramping up of exports is simply leading to economic stagnation, since the core countries (largely net savers) are unable to take up the demand slack.

What makes the country different is that in Japan the cracks are starting to become visible. The positive external balance which is essentially the only source of growth for the economy is quickly evaporating. The trade balance is now well negative in large part because of the continuing need for energy imports (mainly LNG and oil) and this has started to drag the current account down. Even worse the income balance is also now falling lead the country to recently post its lowest current account surplus since 1985.

Seen in the light of the above, these recent trends in Japan’s external balance are deeply worrying.

To become even more worried, let’s get back to the debt.

A Balloon Which Just Grows And Grows

Amazingly, Japan is the only developed economy still expanding its annual budget deficit even though the economy is saddled with, by far, the biggest debt burden – gross government debt is now around 235% of GDP. Now many make light of Japan's economic growth problem since with the 15 to 65 population falling, output per worker is not performing badly. As Paul Krugman so cogently puts it, "you can argue that demographically adjusted, the whole tale of Japanese stagnation is a myth." You could, that is, if it weren't for the growing debt. Simply thinking about GDP per member of the active population is very misleading, since what you need to thing about is the elderly dependency ratio, how many people, that is, each member of that steadily shrinking workforce has to support. This is where the real action is.

Evidently a large chunk of this growing debt problem is demographically related. In fact, since the early 2000s, Japan’s non-social security spending has been reasonably well contained and, at about 16% of GDP in 2010, it was the lowest among G-20 advanced economies. Meanwhile, social security costs have risen steadily due to the steady attrition from population aging. Social security spending rose by 60% between 1990 and 2010, accounting for about half of consolidated government expenditures in 2010. Moreover, a sustained increase in the old-age dependency ratio has implied larger social security payments supported by a shrinking pool of workers, and again this has rapidly deteriorated the social security balance.

As long as the interest rate is close to zero, even sky-high debt seems to be fine. But, as the IMF puts it: "Should JGB yields rise from current levels, Japanese debt could quickly become unsustainable. Recent events in other advanced economies have underscored how quickly market sentiment toward sovereigns with unsustainable fiscal imbalances can shift.”

And the IMF draws a scenario, in which a wrong combination of circumstances at an inopportune moment in time could easily send Japan spiralling to where Italy and Portugal are now: “Market concerns about fiscal sustainability could result in a sudden spike in the risk premium on JGBs, without a contemporaneous increase in private demand. Once confidence in sustainability erodes, authorities could face an adverse feedback loop between rising yields, falling market confidence, a more vulnerable financial system, diminishing fiscal policy space and a contracting real economy".

We’re just now seeing the beginning of this scenario. The average rate of maturity on JGBs is being pushed down due to investors buying the short end in combination with the purchasing program from the BOJ. Where have we seen this before ... oh yes, the eurozone periphery. You try to see what yield Japan would need to pay for for a MARKET based 10y or 30y issuance of a decent size. Our best guess is way, way above its nominal growth and herein of course lies the problem. Japan ran a 10% deficit last year and there are no signs of consolidation in 2013. Meanwhile the current account surplus is starting to play the vanishing man act.

Japan will run out of sufficient savings to buy the whole issue of JGBs by 2016, but the possibilities are the market will respond sooner. If the Japanese government continues to issue debt, the Japanese economy is going to run out of savings to buy the new debt. The share of government debt to total currency and deposits will soon reach close to 100%. At this point of the endgame, there is no way out for Japan: either the central bank or foreigners must take up the bid, or Japan must begin to sell off foreign assets. Markets will price in the endgame before it happens.... then it will be game over!

What does game over mean?

How does a country accept its fate of having no other chance of growing other than simply growing old?

How does a country accept its fate of seeing its private savings evaporate? How can a country get along with the discovery that what was seen as a secure source of private wealth and old-age provision, national government bonds, just dematerializes?

Of course, each country is different, especially if it goes through a heavy crisis. And, at least, over the years the Japanese built up a strong net external investment position which leaves the current account strongly positive despite the negative goods trade balance due to the high income flow from investments abroad. This is very different from Italy and Portugal, countries which have long run both trade and current account deficits and have very poor net external investment positions. But these external assets and the internal savings are distributed differently, and in case of heavy losses on the domestic side – will the Japanese Gerard Depardieus and those leading global companies with large foreign assets still be happy to pay the surcharge needed for elderly care of all those elderly people that lost their savings because they trusted the government?

Or Japanese young people, will they still be prepared to stay and work in a country which may well have some of the highest income tax rates on the planet?

No matter how Japan will act in its battle to survive the endgame, it is going to provide us with a fascinating experiment to follow because whether it succeeds or not will tell us a lot about our own future, and of how the rest of the OECD will cope with the rapidly ageing societies they have in their own back yards.